To say inflation is a hot topic for every business is an understatement. At a rate of 9.1%, where the CPI spiked 1.3% in just one month from May to June, inflation continues to reduce purchasing power across the US. It is the number one concern for over 60% of Americans, taking over from COVID in just a few short months.

To put this in perspective, COVID is now the top worry for only 10% of Americans.

The statistics are staggering, but news headlines don’t necessarily capture the complexities and nuances of the times. We can’t ignore that high inflation comes off the back of the pandemic.

Just as people were starting to regain their personal freedom with the world opening up, they are now facing potential limitations on their financial freedom.

In these inflationary and ever-changing times, the challenge for business leaders and marketers is real. As news headlines repeat messages of inflation and a potential recession, and as businesses deal with rising costs and rising prices, it is only natural that the instinctual response is to bunker down and contract.

However, the exact opposite should be true. History has shown that those businesses that thrive after a crisis, dug deep and found the courage to look for growth opportunities during the crisis.

To navigate inflationary times, businesses need to find the courage to drive growth

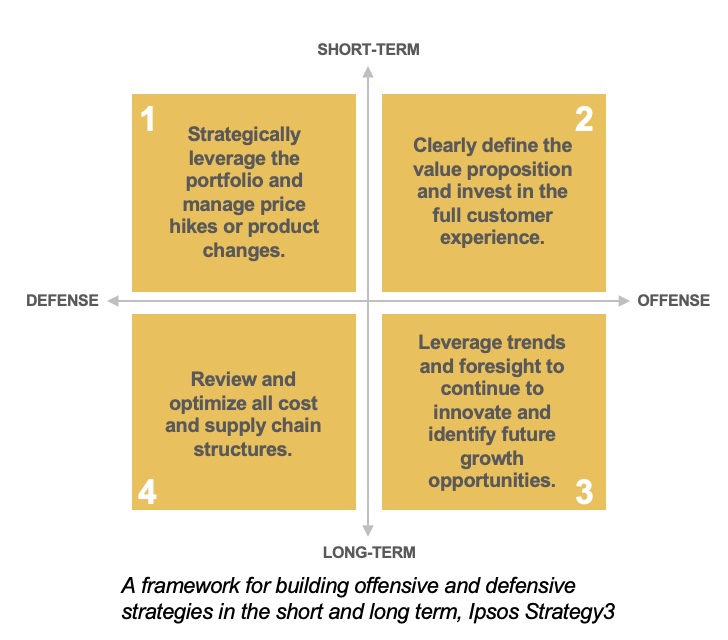

The best strategic approach to drive growth in the current climate is to play offense as well as defense. This means identifying a suite of strategies that not only optimizes costs and pricing, but also adds value to the brand and customer experience, that not only addresses the short-term needs of today, while identifying opportunities for tomorrow as well.

A business mindset of short-term cost cutting and stripping out will stunt future growth – this is a time to add value to the full customer experience

It may seem counter-intuitive to invest in marketing initiatives that enhance the brand and customer experience, at a time when business reality calls for reducing costs and raising prices.

However, if a business mindset becomes one of “stripping out and giving less,” the customer will be left feeling as if they are “receiving less and being undervalued.” This will have detrimental effects in the long-term.

Customer satisfaction will erode first, then loyalty, and finally customers will vote with their feet. This is a time to nurture and cement the customer relationship, not abandon it.

Managing costs and pricing on the left side of the ledger not only needs to be handled with care, but it needs to be balanced with adding value on the right side of the ledger.

Uber vs. The Yellow Cab: a case in eroding customer loyalty in a crisis

One only needs to read Twitter comments on Uber vs. The Yellow Cab in New York City for this to ring true. Uber’s surge pricing seemed to skyrocket during the pandemic. But as fuel prices escalated at the beginning of this year, what is usually a $15 ride across town was being quoted at nearly three times this.

If the fuel prices were justification for this increase, why was the same not true of Yellow Cab prices? With no brand communication to explain why, and a cheaper alternative, social media was the perfect platform for people to air their negative sentiment towards Uber.

Hyundai Assurance: a case in innovating to meet consumer needs in a crisis

In contrast, consider the launch of Hyundai Assurance during the 2009 recession. With marketing messages around “creating certainty in uncertain times”, Hyundai removed the risk of purchasing a car.

The first of its kind, Hyundai Assurance was launched as a buy-back program. New-car buyers and lessees who involuntarily lost their jobs within the first year of purchase, could sell back their vehicle up to a certain value. It is a perfect case study in staying vigilant about consumer needs in a time of crisis and innovating to meet them.

When purchasing power is shrinking, and financial pressure on consumers filters down to financial pressure on businesses, it is understandable to want to spend less on the customer experience. Doing the opposite – especially in a way that shows empathy for the moment – will go a long way.

Long-term planning is key to setting a business up for success post crisis

While businesses will need to deploy tactics in the short term to respond to the immediate priorities of the day in the constantly changing landscape, foregoing all long-term planning and innovation is short-sighted.

To quote Harvard Business review, “Companies that fared the best during crises were the most progressive ones – with substantial investments into R&D and marketing – resulting in a +37% chance of becoming industry leaders following recession.”

Apple: a case in investing during downturns

When the dot-com bubble burst in 2001, Apple’s response was to increase its investment in innovation. It was this courage to drive growth, even during a downturn – and the downturns that followed – that truly drove its success.

The iPod was released in 2001 and iTunes in 2003. The launch of the iPhone in 2007 saw stock prices jump 15.9%. The launch of the iPad in 2009 saw an increase of 40%.

Apple’s continued innovation through one financial crisis after another, has helped the business not only weather the storms, but emerge stronger after the storms have passed.

We can’t predict the future, but we can prepare for it

As this article began, the only constant is change. Not only are we in the midst of great economic uncertainty, but we are experiencing significant change on top of significant change: a pandemic, political instability, supply chain disruptions, an ever-evolving workforce, and now a question mark that hangs over a possible recession.

However tempting it is to respond to these fluctuations by focusing on securing the bottom line for the short-term, business leaders cannot forgo the importance of future-proofing their businesses for the long-term. In order to do so, there is no one-size-fits-all solution.

In the past few months, data has shown that every market, every brand, and every consumer group respond differently. And so, this is a time for every business to intimately know the nuances of its market, its brand, and its consumers. Using this information, a business can leverage a suite of strategies, across the board, to drive growth now and into the future.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.OkNoPrivacy Policy

: Maximise Your Price Elasticity.")