One month into the release of iOS14.5, a report by Flurry (a Verizon owned measurement firm) showed that only 13% of users globally have opted in to allow apps to track them via IDFA. The same opt-in rates for the US are an abysmal 5%. For advertisers, while the opt-in rates are as expected, it is still met with a sense of dread. Concepts that advertisers have gotten comfortable with (e.g., ad targeting, ad measurement, conversion tracking) are now impacted, and advertisers are having to scramble for alternatives.

Coupled with the impending depreciation of 3rd party cookies and a growing movement of politicians wrangling antitrust lawsuits against duopoly Facebook and Google, the current landscape has inadvertently given rise to a whitespace for advertisers who are looking for more value from their partners. In Asia, the solution is being found in super-apps.

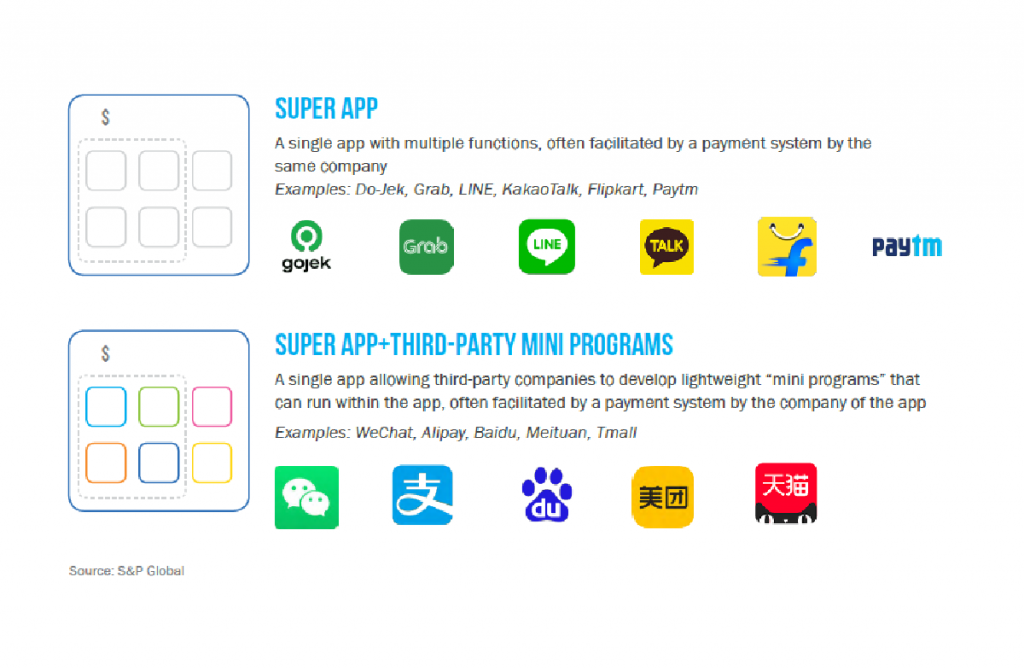

Super-apps and their ability to enable deeper partnerships

Having amassed huge user bases, super-apps like Grab, Gojek, Kakao, and PayTM are now in the unique position to offer advertisers access to richer audience data, formats, and attribution. Many of these super-apps are willing to invest in longer-term strategic partnerships and offer the ability to facilitate partnerships within its network, proving their commitment to advertisers – a stark contrast to the transactional nature of ad buying on Facebook and Google.

It is predicted that Grab’s ad revenue might come up to $245m, or 10% of its total revenue. This is achieved via its capabilities in direct-to-consumer communication and enabled by its rich bank of signal-based transactional data collected across its plethora of offerings. The act of targeting consumers based on their transaction data, which remains unshaken by restrictions on IDFA, gives them a deterministic way to reach consumers and bridge online-to-offline journeys.

Furthermore, Grab’s willingness to facilitate partnerships by integrating brands in every part of the business journey (from ad formats to payment options and collection/delivery) is rooted in the commitment to delivering business outcomes for brands.

The same can be observed with PayTM, India’s biggest mobile payments platform, and their advertising solutions. With payment information from a strong 600m user base paired with consumer transaction data, PayTM can offer advertisers partnerships that transcend advertising formats.

In a recent campaign, Visa worked with PayTM to push users to register for Visa Safe Click – a programme that allowed for more seamless payments and higher transaction limits. The enhanced partnership included the development of brand stores, customer incentives, and platform-wide integrations with the Visa Safe Click messaging being shared to pre-qualified audiences based on prior transaction details. The coming together of robust 1st party data and customized offerings offered up value to the brand that only a super-app could do.

Where does this leave us?

Make no mistake, ad spends, and Facebook and Google’s dominance in the region will continue to grow in tandem with the growing digital dollar. However, we will also see significant increases in spending or even investments with the super-apps as advertisers look for new and different ways to connect with their consumers.

Behaviours like that of ‘search’ will become more specific and move into the super-apps. With the apps increasingly assimilating into everyday life, consumers will look less to Google to find information and go straight into the apps for answers. This will shorten the direct-to-consumer path and force advertisers to reconsider how to reach their consumers more quickly with the help of these super-apps.

Looking North

One lacking element on super-apps like Grab, Gojek and PayTM is social. Whether this is something to be integrated one day or a function to be captured by other verticals of super-apps, one should look to China’s tremendous ecosystem of super-apps as a reference.

In the past few years, China has exploded with super-apps that allow for third-party mini programme integration. These lightweight ‘mini programmes’ are found within the app and launched through the main app’s interface. WeChat itself holds over 2.4 million mini-programmes that consist of news, mobile payments, e-commerce shops, food delivery, and social. This implies a reducing needs for developers/businesses to need to own an app but instead tap on the super-app to acquire users and drive usage.

As we move into the next few months, the industry will be deep in the troughs of simultaneously figuring out the effects of iOS14.5 restrictions while arming themselves for the impending cookie depreciation. For advertisers, it is a good time to consider how the super-app ecosystem in their markets could fit into their overall strategies and enhance the way they connect with consumers.